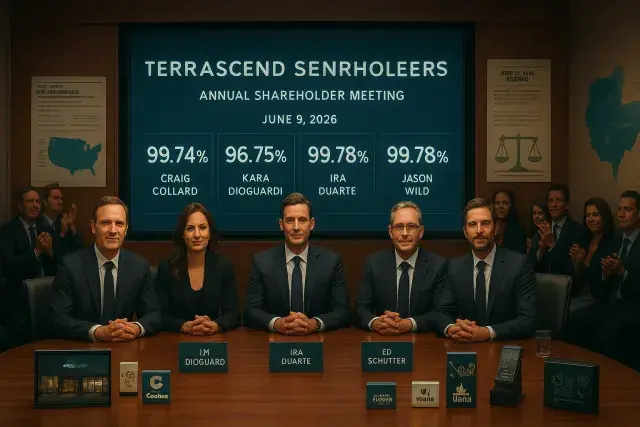

At its annual meeting held June 9, 2026, TerrAscend Corp. secured shareholder approval on every resolution put to a vote - director re-elections, auditor ratification, and renewal of its equity compensation plans - each passing with support above 99 percent of shares cast. For a multi-state cannabis operator managing licensed operations across Pennsylvania, New Jersey, Maryland, Ohio, and California, that level of governance continuity carries real operational weight.

The five-member board - Craig Collard, Kara DioGuardi, Ira Duarte, Ed Schutter, and Jason Wild - was returned intact, with individual approval rates ranging from 96.75 percent for DioGuardi to 99.74 percent for Collard. That stability matters in a sector where regulatory standing is tied directly to the individuals named on licenses. In states like Maryland, where the adult-use market has required operators to maintain tight compliance infrastructure - including technology capable of meeting seed-to-sale reporting obligations - board continuity signals to regulators and investors alike that the compliance chain of command isn't changing. Operators in that market tracking technology investments, including dispensary pos maryland solutions built for state-specific compliance requirements, understand that leadership consistency at the corporate level often correlates with more predictable operational execution at the store level.

Shareholders also ratified MNP LLP as the Company's auditor for the fiscal year ending December 31, 2026, with 99.78 percent of shares voting in favor. Auditor continuity is quietly significant in cannabis - operators subject to both state-level financial reporting requirements and the ongoing constraints of 280E (or its post-rescheduling successors) need accounting firms with actual cannabis-sector depth. MNP, a Canadian firm with established cross-border cannabis audit experience, has served TerrAscend in that capacity, and retaining them signals no disruption to financial reporting infrastructure heading into what remains a complex regulatory year.

Equity Plans Pass, Reflecting Ongoing Talent Pressure Across the Sector

The two equity compensation resolutions - covering unallocated stock options under the Company's stock option plan and unallocated share units under its share unit plan - each cleared 99 percent approval. That's worth pausing on. Cannabis operators have long faced a structural disadvantage in attracting senior finance, legal, compliance, and operations talent: federally chartered banks won't touch cannabis equity as collateral, and the stigma that once shadowed the industry hasn't fully dissolved in executive recruiting markets. Stock options and share units are among the few tools a publicly listed cannabis company can use to compete with conventional industries for experienced professionals.

The approval of unallocated units doesn't mean those instruments are issued - it means the board has the authority to grant them without returning to shareholders each time. That's standard practice for public companies, but in a cannabis context it also reflects how quickly compensation decisions sometimes need to move, particularly when a company is staffing up a new market, responding to a licensing event, or replacing compliance leadership.

Rescheduling Still an Open Question - and TerrAscend Said So Directly

The Company's regulatory disclosure accompanying the meeting results is unusually candid, and worth reading closely. TerrAscend notes that on April 23, 2026, the U.S. Department of Justice issued a final rule rescheduling marijuana in FDA-approved drug products and marijuana subject to a state medical marijuana license from Schedule I to Schedule III of the Controlled Substances Act. That's a meaningful but narrow move. Any cannabis that doesn't fit those two categories - which covers the vast majority of adult-use product sold across TerrAscend's dispensary network - remains a Schedule I controlled substance under federal law.

A broader rescheduling hearing is scheduled to begin June 29, 2026, covering all marijuana from Schedule I to Schedule III. TerrAscend's disclosure is explicit: no final action has been taken, and there is no assurance as to timing or outcome. The company also reaffirms what operators across the industry already know - that state-law compliance does not constitute a federal defense, and that financial transactions involving cannabis-related proceeds remain subject to federal money laundering risk. Plain language, no hedging. That's the kind of disclosure that operators, investors, and compliance officers actually need to read in full.

The thing is, rescheduling to Schedule III - even in its broader proposed form - does not federally legalize adult-use cannabis. It changes the drug's regulatory classification for controlled substance purposes, potentially opens certain research pathways, and could affect how 280E applies to cannabis businesses. But it doesn't resolve banking access, interstate commerce restrictions, or the fundamental tension between state-legal operations and federal prohibition. TerrAscend's caution language reflects exactly that reality.

What This Means for Operators Watching TerrAscend's Footprint

For dispensary owners, wholesalers, and technology vendors operating in the markets where TerrAscend competes - New Jersey's competitive adult-use environment, Pennsylvania's still-evolving regulatory structure, Maryland's post-legalization market - the governance stability confirmed at this meeting has direct implications. Multi-state operators with stable boards and ratified auditors tend to be more predictable counterparties: more consistent in their wholesale purchasing behavior, more reliable in their compliance documentation, and less likely to create disruption downstream in the supply chain.

TerrAscend's brand portfolio - which includes The Apothecarium dispensary locations, Cookies, Kind Tree, State Flower, and Wana, among others - spans cultivation, processing, manufacturing, and retail across its core markets. Keeping the same board in place heading into the second half of 2026 means the strategic decisions already in motion - around pricing, SKU management, market positioning, and capital allocation - are unlikely to face abrupt recalibration. In a sector still operating under significant regulatory and financial uncertainty, that predictability has real commercial value.